It’s only January and there’s so much to consider as the housing market gets rolling in 2023. In June 2022, interest rates started to rise in an attempt to curb inflation, causing a seismic shift in the housing market across the nation. We are in the “after June 2022” times now…

Pre June 2022, the story was historically low interest rates, high buyer demand, soaring appreciation, bidding wars, and outright mayhem. Then inflation snuck its way onto the scene and the Fed had no choice but to step in and do something to tame it. In the second half of 2022, we saw the Fed raise rates faster than any other time in history. With this rise in rates, we saw the return of housing inspections and appraisals (hallelujah), but alas buyers are still facing bidding wars! What’s the deal with that?

That’s where we will see more similarities between 2022 and 2023 than you might be thinking. It all boils down to inventory. We feel like a broken record here, but we continue to harp on the same three important data points. Here is what we said last year in detail, but if you don’t feel like reading more, here’s a quick recap.

2022 Recap

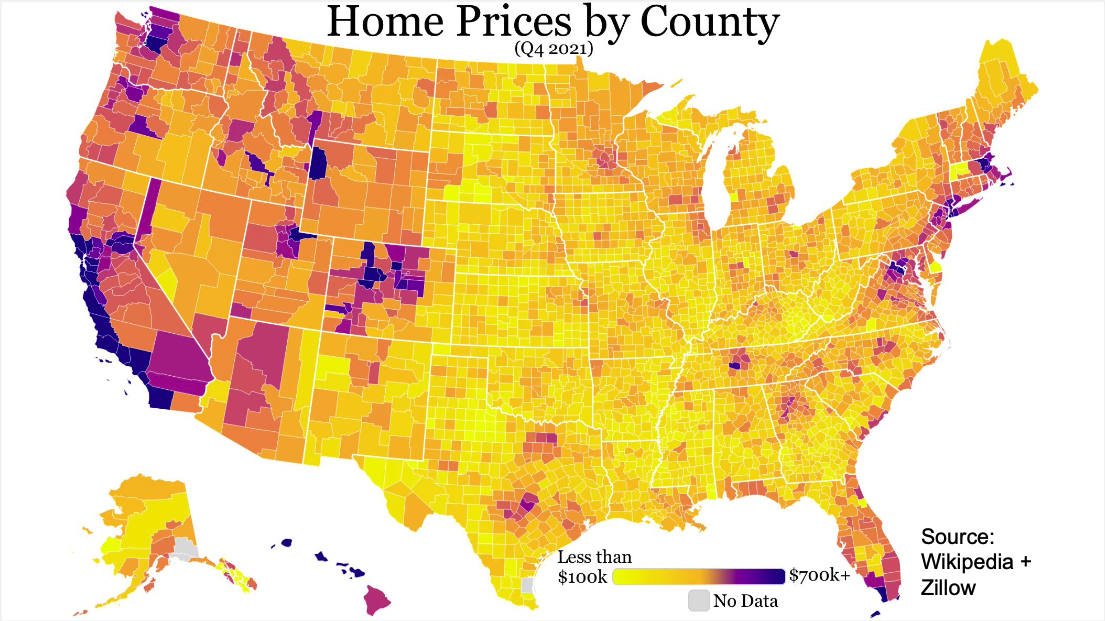

#1: RVA is Cheaper than Most Everything North

#2: Thanks to #1, People Continue to Migrate to RVA

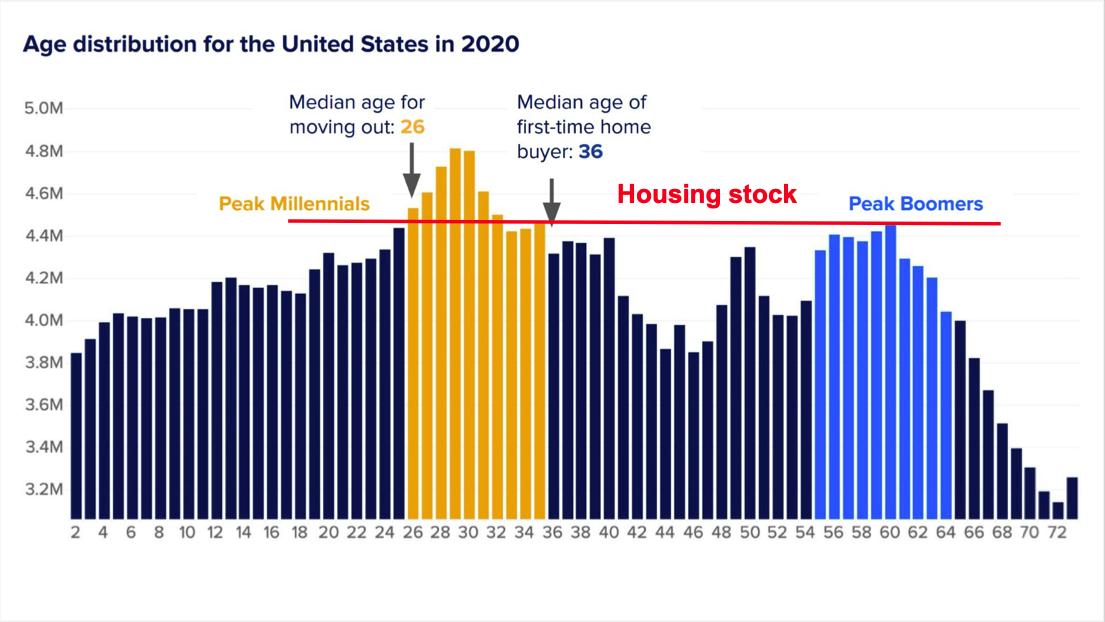

#3: The Millennials are Ready to Buy

The Millennial population is the largest generation ever and the biggest chunk of millennials are just now hitting the average age of first-time home buyers (33-36 years old).

These three factors (and historically low mortgage rates prior to June 2022) are what have been driving the Richmond inventory down for years. Lots of folks point to COVID as the driving force, but COVID, and the resulting change in the work from home and migration patterns, was really the accelerator. Richmond has seen decreasing inventory since 2012 and reported bidding wars as early as 2015.

Interest Rates and the Lock-in Effect

Thankfully, inflation seems to be moderating. This should:

- Have a positive impact on rates. Housing is extremely sensitive to interest rates.

- Rates should continue to improve if inflation continues to slow down (theoretically).

Molly Boesel, Principal Economist with Core Logic, reports the median mortgage rate on outstanding mortgage debt is 3.1%. “One reason that fewer owners are putting their homes on the market is because of something called the ‘lock-in effect.’ Homeowners who hold low-interest-rate mortgages are reluctant to sell in an environment with rising rates because that means relinquishing the low mortgage rate on a current property and taking out a higher-rate mortgage on a new purchase.”

Affordable Housing

In an article written in March 2016 about Richmond and Affordable housing, Rick Jarvis states, “So while our problem feels smaller than their (DC, NY, SF) problem, just remember that their problems used to be a lot smaller, too, until they weren’t.” Rick went on to say, “When we ignore the issues, we do so at our own peril and while our affordable housing problem is not our biggest problem – yet – the stage is set for it to not only become far more problematic in the near future, but far harder to cure as well.” Some contributing factors to lower and lower affordable housing includes:

- In 2020, new construction represented 1 in 5 available homes between $250,000 and $400,000. In 2022 that ratio is now 1 in 19.

- In December 2022 there was 0.8 months of inventory in the Richmond Metro on homes priced below $450,000. That’s only 543 “affordable” homes available for sale under $450,000 in a Metro area of 1.1 million people.

Side note: Renting is not an affordable option either.

2023 Predictions

In 2023, we believe that inventory is still going to be tight, keeping the power in sellers’ hands, although they won’t wield as much power as they have in the last 3 years as the market starts to become more “normal”.

Inventory

Inventory will remain low across all price points. Compared to the Northeast, Richmond is a “bargain buy”. Other factors like large millennial buying pools, the high costs of new construction and the interest rate “lock-in effect” will keep inventory low, too.

Home Prices

Richmond homes prices will remain stable. Especially at entry level price points below $500,000. Additionally:

- The large media markets to the North and West are experiencing negative migration and have been overbuilt. Prices will moderate and/or fall in some cases in those areas as more people migrate to Richmond.

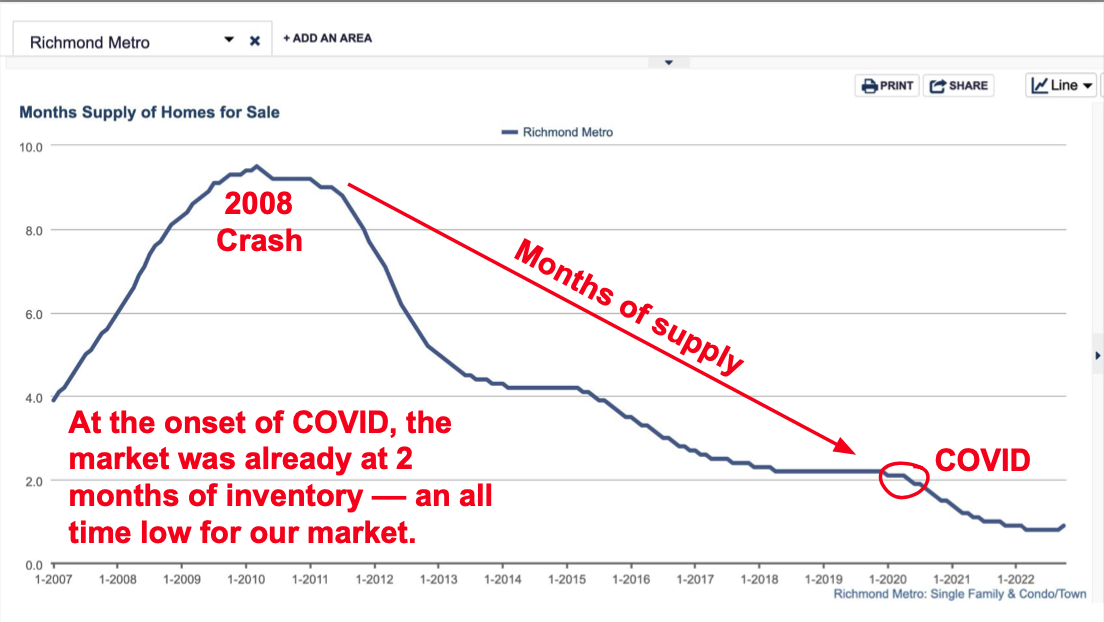

- Prices tend to fall when inventory reaches 7 months. Right now, resales are still under 2 months of inventory (check out that blue line below).

Interest Rates

Predicting rates is a fool’s game, but so far the Fed seems like they are pulling off the great balancing act they were shooting for. For that reason, we feel inflation will continue to cool and we will see rates consistently in the 5% range and potentially creep down. We reserve the right to be wrong on this since it seems like the federal government’s left hand rarely knows what the right hand is doing, so naturally things could go sideways.

New Construction

Builders have already drastically slowed production. This trend will continue until the cost of building comes down. Without a miracle breakthrough in construction techniques or significant legislation changes, the cost of building a home won’t go down any time soon.

Fear Has it’s Place

Fear is warranted in many scenarios throughout our lives. For example, just before you jump out of a plane. Walking down a dark alley. Free climbing. However, fear shouldn’t be a factor when make the largest investment in your entire life. Don’t let the doom and gloom media headlines sway your home buying/selling decisions. Sometimes those headlines are right; some housing markets will be slow in 2023, but Richmond won’t be one of them.

Let’s Get Started

Want to dig in more? We are here for you. Let’s grab a beer or coffee!